This content originally appeared on HackerNoon and was authored by DeLeverage

Table of Links

3 Background

4 System Model and 4.1 System Participants

4.2 Leverage Staking with LSDs

7.1 stETH Price Deviation and Terra Crash

7.2 Cascading Liquidation and User Behaviors

8 Stress Testing

8.1 Motivation and 8.2 Simulation

9 Discussion and Future Research Directions

A. Aave Parameter Configuration

B. Generalized Formalization For Leverage Staking

C. Leverage Staking Detection Algorithm

4 System Model

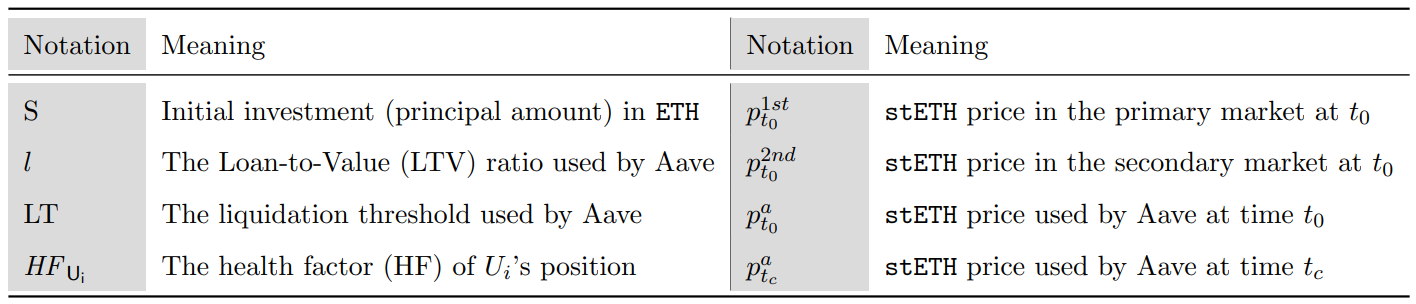

We first provide a set of notations to facilitate the understanding of related equations.

\

4.1 System Participants

We consider an LSD ecosystem on the Ethereum blockchain with the following participants.

\

\ Liquid Staking Providers: Ui can stake native tokens (e.g., ETH) on liquid staking platforms (e.g., Lido) to receive LSDs (e.g., stETH). These derivatives can then be used in various financial activities, including trading, collateralized borrowing, and liquidity provision.

4.2 Leverage Staking with LSDs

This section introduces and compares three strategies: (i) leverage borrowing, (ii) direct leverage staking, and (iii) indirect leverage staking strategies.

\

\

\ \ 4.2.1 Leverage Borrowing

\ In the context of Etherem, particularly prevalent in its PoW phase, “leverage borrowing” emerges as a commonly adopted strategy. This process involves users initially exchanging asset X for Y within a DEX pool. Subsequently, asset Y is supplied as collateral on lending platforms to borrow asset X. This borrowed asset X is then exchanged again for Y in the DEX pool, enabling users to iteratively amplify their leverage borrowing positions.

\ The financial incentive behind the leverage borrowing strategy lies in the user’s ability to expand the deposit-borrow leverage by repeatedly cycling through swapping, depositing, and borrowing. Although the deposit rate offered by the lending platform is lower than the borrowing rate, the larger total amount of asset Y deposited compared to asset X borrowed typically results in net earnings, which can be further amplified through leverage.

\ 4.2.2 Leverage Staking

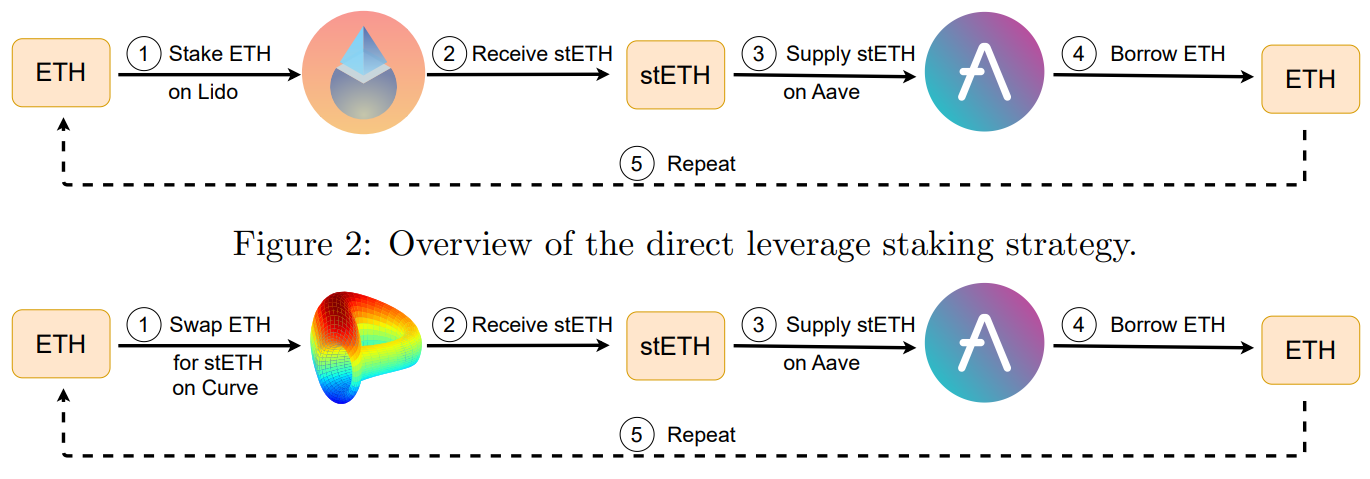

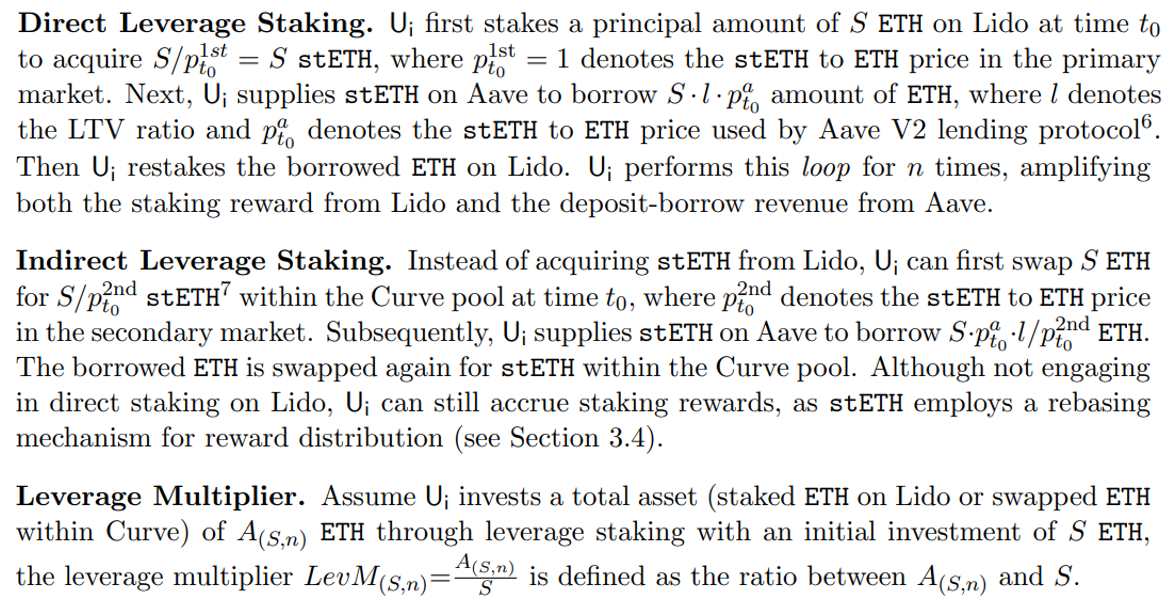

\ Following the introduction of PoS staking, a concept analogous to leverage borrowing, termed “leverage staking”, has emerged. It is a strategy intricately linked with LSDs and involves a recursive cycle of staking/swapping, depositing, and borrowing (see Figure 2 and 3) to increase financial returns. We concentrate our analysis on leverage staking within the Lido– Aave–Curve ecosystem and describe direct and indirect leverage staking as follows.

\

\

\

\

\

\ \ Direct vs Indirect Leverage Staking. Both direct and indirect leverage staking strategies are designed to amplify staking rewards through a recursive methodology. However, direct leverage staking acquires stETH from the LSD primary market, whereas indirect leverage staking obtains stETH from the secondary market. Notably, indirect leverage staking bypasses the staking process, consequently not contributing to the increase in the total staked ETH within the network. Utilizing the same principal amount of ETH, Ui generally acquires more stETH through the indirect strategy, as the stETH to ETH price in the secondary market is often below 1. However, this approach incurs additional costs associated with swaps and is susceptible to potential price slippage, often exacerbated by front-running activities.

\ Leverage Staking vs Leverage Borrowing. While leverage staking and leverage borrowing both exhibit recursive patterns, they diverge for several reasons. Firstly, leverage staking primarily targets LSDs, whereas leverage borrowing is focused on non-LSD tokens. Secondly, leverage staking aims to amplify both staking rewards and the deposit-borrow revenue, while leverage borrowing solely seeks to enhance the deposit-borrow revenue (see Table 2). Third, they bear different risk sources. In addition to market risk, leverage staking involves the risk of slashing (see Section 3.2). To summarize, although the traditional leverage borrowing strategy shares some similarities with the leverage staking strategy discussed in this paper, they differ in terms of underlying assets, income sources, and associated risk.

\

:::info Authors:

(1) Xihan Xiong, Imperial College London, UK;

(2) Zhipeng Wang, Imperial College London, UK;

(3) Xi Chen, University of Sussex, UK;

(4) William Knottenbelt, Imperial College London, UK;

(5) Michael Huth, Imperial College London, UK.

:::

:::info This paper is available on arxiv under CC BY 4.0 DEED license.

:::

\

This content originally appeared on HackerNoon and was authored by DeLeverage

DeLeverage | Sciencx (2025-07-08T05:18:43+00:00) Comparative Analysis of Leverage Borrowing and Leverage Staking in Ethereum’s LSD Ecosystem. Retrieved from https://www.scien.cx/2025/07/08/comparative-analysis-of-leverage-borrowing-and-leverage-staking-in-ethereums-lsd-ecosystem/

Please log in to upload a file.

There are no updates yet.

Click the Upload button above to add an update.